Geopolitics & Global Markets

On Massive Life Support

How a fragile ceasefire between the United States and Iran became the most consequential variable in global energy markets — and what traders need to understand about the forces keeping it alive.

On the morning of 12 May 2026, President Donald Trump told reporters gathered in the Oval Office that the monthlong ceasefire between the United States and Iran was on “massive life support.” He described it as “unbelievably weak,” while insisting it technically remained in force. The words landed with the weight of a man who had built his public identity on the deal, and who was now watching it fray in real time. For anyone with exposure to energy markets, commodity trades, or risk assets of almost any kind, those six words carried the force of a price alert.

The conflict that produced this ceasefire did not begin in April. It has its roots in a diplomatic failure stretching back over a year, through rounds of indirect talks, missed deadlines, and ultimately a joint US–Israeli military campaign that reshaped the security architecture of the Middle East. Understanding the ceasefire — its origins, its terms, its fragility, and its market implications — requires understanding the full arc of events that brought both sides to this precarious moment.

How the War Began

The immediate origins of the 2026 Iran conflict trace back to April 2025, when President Trump sent a letter to Iranian Supreme Leader Ali Khamenei proposing nuclear negotiations with a sixty-day deadline. The first round of high-level discussions took place in Oman that same month, led on the American side by special envoy Steve Witkoff and son-in-law Jared Kushner, and on the Iranian side by Foreign Minister Abbas Araghchi. Further rounds followed in Rome and Muscat, with both sides describing the discussions as “constructive” while privately acknowledging deep disagreements.

The central fault line was uranium enrichment. Washington demanded zero enrichment — the complete dismantlement of Iran’s nuclear infrastructure. Tehran refused categorically, insisting on its right to enrich for civilian purposes. By the time a third round concluded in Geneva in February 2026, American officials were privately conceding that the talks had reached an impasse. The Wall Street Journal reported that Witkoff and Kushner had told Trump it would be “difficult, if not impossible,” to reach a deal through diplomacy. According to analysts at the Arms Control Association, by the time the Geneva session ended, Trump had likely already made the decision to go to war.

On 28 February 2026, the United States and Israel launched large-scale co-ordinated strikes against Iranian military leadership, nuclear scientists, and the country’s three principal nuclear sites: Fordow, Natanz, and Isfahan. Supreme Leader Ali Khamenei was killed in the strikes. Iran immediately suspended all nuclear talks and declared the Strait of Hormuz closed to international shipping.

The consequences were immediate and seismic. Beginning on 4 March 2026, Iranian Revolutionary Guard Corps forces deployed mines, drones, missiles, and fast-attack craft throughout the strait, threatening any vessel attempting transit. Within days, shipping firms suspended operations entirely. Brent crude surged past $120 per barrel. QatarEnergy declared force majeure on all exports. Collective oil production across Kuwait, Iraq, Saudi Arabia, and the UAE dropped by an estimated 6.7 million barrels per day by 10 March. The International Energy Agency characterised what followed as the largest supply disruption in the history of the global oil market — a shock that analysts compared to the 1970s energy crisis in its capacity to generate acute stagflation across advanced economies.

— INSERT IMAGE BLOCK HERE —

A wide aerial or satellite-style graphic of the Strait of Hormuz with shipping lanes marked, or a striking photojournalistic image of an oil tanker convoy in the Persian Gulf under grey skies.

The Ceasefire and Its Terms

By late March 2026, Pakistan had emerged as the key mediating power. On 25 March, Pakistani officials delivered a fifteen-point American proposal to Tehran that included an end to Iran’s nuclear programme, limits on its ballistic missiles, the full reopening of the Strait of Hormuz, restrictions on Iranian support for armed groups, and sanctions relief in return. Iran rejected it. The Iranians issued a five-point counter-proposal demanding an end to US–Israeli attacks, security guarantees against future aggression, war reparations, and international recognition of Iranian sovereignty over the Strait. Washington dismissed this as non-negotiable.

On 7 April 2026, Trump announced on Truth Social that he had agreed a two-week ceasefire with Iran, mediated by Pakistan. The announcement came after Iran itself had proposed a ten-point alternative framework, having already rejected Pakistan’s draft forty-five-day plan. At an 8 April press conference, Trump framed the pause in expansive terms, suggesting the United States would “work closely with Iran” on tariffs, sanctions, and uranium removal. Vice President JD Vance, standing beside him, described it more bluntly as a “fragile truce.”

The ceasefire did not bring silence. Both sides fired on each other in the Strait of Hormuz in the days that followed. The UAE reported Iranian drone and missile attacks on two consecutive days in early May. A French shipping vessel, the CMA CGM San Antonio, was attacked while transiting the strait, injuring crew members. By 10 March, only fifteen ships had made it through the passage that had previously carried a fifth of the world’s seaborne oil trade. The United States responded on 13 April by imposing a naval blockade on Iranian ports — a move Iran described as a potential “prelude to a violation of the ceasefire.” Neither side lifted its blockade.

The One-Page Framework

By early May 2026, the shape of a possible longer-term deal had begun to emerge from behind the noise of public threats and diplomatic manoeuvring. Axios reported on 6 May that the White House believed it was closing in on a one-page, fourteen-point memorandum of understanding with Iran — the closest the two sides had come to an agreement since the war began. The MOU was being crafted by Witkoff and Kushner in both direct and indirect negotiations with Iranian officials, with Islamabad and Geneva both floated as venues for what would follow.

In its reported form, the MOU would declare an end to the war and open a thirty-day period of detailed negotiations on three core issues: Iran’s nuclear programme, the lifting of US sanctions, and freedom of navigation through the Strait of Hormuz. Iran would commit to never seeking a nuclear weapon and to an enhanced inspections regime, including snap inspections by the International Atomic Energy Agency. Underground nuclear facilities would be shut. Crucially, Iran would agree to export its stockpile of highly enriched uranium — a demand Tehran had consistently rejected throughout the preceding year’s diplomacy, and one source suggested the material would be moved to the United States. For its part, Washington would commit to a gradual lifting of sanctions and the release of billions of dollars in Iranian funds frozen around the world. Both sides would progressively ease their blockades in the Strait of Hormuz during that thirty-day window.

The duration of the uranium enrichment moratorium remained the principal unresolved clause. Three sources told Axios that twelve years was the floor; one suggested fifteen was the likely landing point — a compromise between Iran’s preferred five-year limit and Washington’s original demand of twenty. After the moratorium, Iran would be permitted to resume enrichment at 3.67 per cent — precisely the level permitted under Barack Obama’s 2015 Joint Comprehensive Plan of Action. Analysts at Slate noted the irony: the deal Trump’s administration tore up in 2018 appeared, eight years and one war later, to be the template his envoys were now reconstructing.

— INSERT IMAGE BLOCK HERE —

A photojournalistic image of diplomatic talks in progress — negotiators at a table, or envoys arriving/departing an airport, ideally in Islamabad or Oman. Alternatively, a striking image of Trump at the Oval Office desk with a tense expression.

Why It Collapsed Again

The MOU never landed. Iran’s response, when it came, was described by Trump on 11 May as “totally unacceptable” and “stupid.” The specific point of collapse centred on the fate of the enriched uranium buried beneath the bombed nuclear sites. Trump told reporters from the Oval Office that Iran had privately indicated it would hand over the material — but that the United States would need to physically come and remove it. “They told me, number one, you’re getting it, but you’re going to have to take it out,” he said. Then, within days, that offer was withdrawn, apparently because it had never been formally committed to in writing. “They changed their mind, because they didn’t put it in the paper,” Trump said.

Equally critical was what the Iranian letter omitted: a clear commitment that Tehran would never seek a nuclear weapon. “I have a great plan,” Trump told reporters, “but the plan is they cannot have a nuclear weapon. And they didn’t say that in their letter.” Without that explicit renunciation, the White House saw no basis for progress.

Trump’s characterisation of the Iranian side as divided between “moderates” and “lunatics” offered a window into his read of the situation. The moderates, he said, were “dying to make a deal” but were constrained by hardliners within the Revolutionary Guard and the clerical establishment who preferred to continue fighting. This internal fissure in Iranian decision-making has been a recurring theme in the talks: at the Islamabad session in April, key Iranian figures including parliamentary speaker Mohammad Bagher Ghalibaf declined to attend at all, citing a lack of trust. When Vance and Witkoff returned to Islamabad a second time, they left without an agreement.

Meanwhile, the pressure on the ceasefire from below continued to build. Iran’s Revolutionary Guard captured the MSC Francesca in the Strait of Hormuz, underscoring that the formal truce had not translated into operational calm on the water. Iran’s counter-blockade — targeting ships attempting to access Iranian ports from 13 April onwards — remained in force. The dual-blockade dynamic had reduced throughput to a trickle compared with pre-conflict levels. The US, for its part, briefly announced then backed away from a new escort operation in the strait after progress was reported in back-channel talks — a signal that Washington understood the commercial stakes well enough to hold back from full escalation.

Reading the Market Signals

For traders, the relationship between headline news and price movement in this conflict has been both instructive and treacherous. Oil markets have responded sharply to every significant development since the first strikes in February — but the directionality has been far from uniform, and the speed of reversals has punished those who entered positions on pure sentiment.

Following the April ceasefire announcement, Brent crude dropped 1.2 per cent to $108.60 a barrel, with West Texas Intermediate falling in parallel to $101.06 — reflecting the market’s relief that the strait might reopen. A further 4 per cent decline followed in subsequent sessions as diplomatic optimism built around the MOU framework. But those gains were partial and unstable. Brent had already surged above $120 in the weeks before the ceasefire; the so-called “risk premium” baked into prices was never fully eliminated, because the strait never fully reopened. As of 12 May, with Trump publicly declaring the ceasefire on “massive life support,” that premium has re-entered the equation with force.

— INSERT IMAGE BLOCK HERE —

A custom div-based chart showing Brent crude price movement from January 2026 through May 2026, illustrating the surge on 28 February, peak above $120, and partial relief after the ceasefire. (See chart block below.)

$120

$110

$100

$90

$80

$70

The gold market has moved in parallel with crude, if with a somewhat different character. Gold prices rose consistently throughout the early weeks of the conflict as investors sought safe-haven exposure. The nuclear dimension of the conflict — specifically the prospect of Iran reconstituting weapons-grade capability — added a tail-risk premium that conventional inflation-hedge demand alone would not have justified. When Trump described the ceasefire as on “massive life support,” gold moved higher again in Asian trading the following session.

For equity markets, the picture is more nuanced. European equities with heavy energy sector weightings have experienced elevated volatility, as have UK-listed oil majors BP and Shell, both of which carry significant exposure to Middle Eastern supply chains. The FTSE 100’s energy component has tracked the conflict’s news cycle closely — a reminder that even a domestically focused index portfolio carries meaningful indirect geopolitical risk through its sector composition. Shipping and logistics equities have been hit hardest of all: the cessation of strait transit has fundamentally disrupted route economics for vessels ordinarily serving the Gulf, the Indian subcontinent, and East Asia through the Persian Gulf corridor.

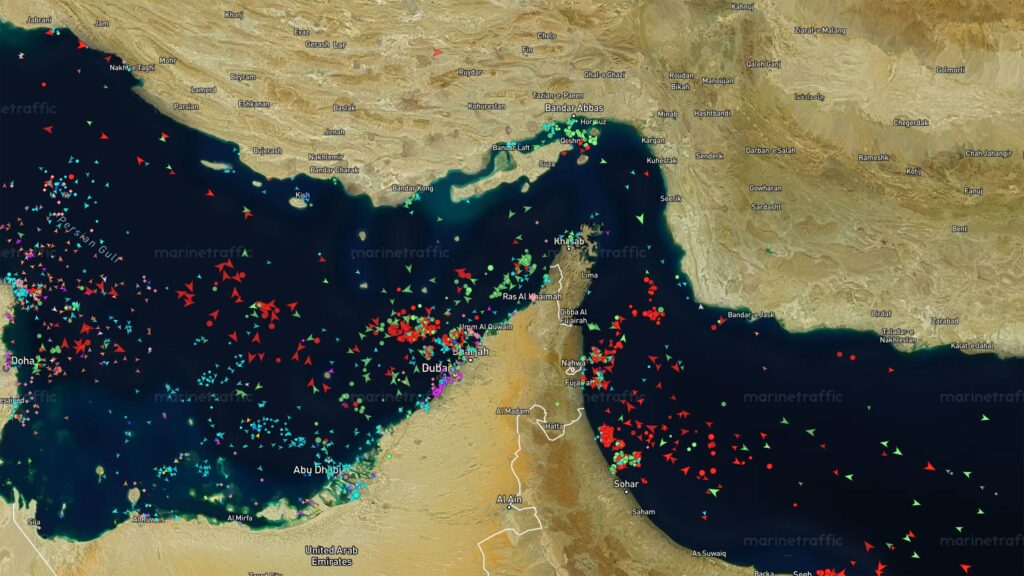

The Strait of Hormuz: Why It Matters to Markets

Before the conflict, the Strait of Hormuz handled approximately 20 per cent of the world’s seaborne oil trade and 20 per cent of global liquefied natural gas exports. The waterway is just 34 kilometres wide at its narrowest point, making it both irreplaceable as a transit route and extremely difficult to defend at scale. Its closure did not merely tighten supply — it severed the export infrastructure of Kuwait, Iraq, Bahrain, Qatar, and the UAE alongside Iran’s own production. QatarEnergy’s force majeure declaration effectively froze a substantial portion of Europe’s winter gas supply pipeline at a stroke. The IEA described the resulting disruption as the largest in the oil market’s history.

How to Trade This Environment

Geopolitical crises of this nature present traders with a specific set of challenges that differ fundamentally from those posed by macroeconomic cycles, earnings seasons, or monetary policy shifts. The variables are non-quantitative, the timelines are unpredictable, and the key decision-makers are individuals whose behaviour does not map cleanly onto models or historical analogues. That said, frameworks exist for navigating these environments, and traders who understand the structural forces at play are better positioned than those reacting purely to headlines.

The first discipline is distinguishing between signal and noise in the news flow. The US–Iran situation has generated an extraordinary volume of both. Trump’s own public statements have oscillated between threatening resumed bombing and signalling genuine diplomatic optimism within the same press conference. Iranian officials have simultaneously described the talks as progressing and as fundamentally deadlocked. Traders who have taken directional positions based on any single statement have frequently found themselves on the wrong side of the next reversal. The more useful approach is to track structural indicators — shipping throughput in the strait, the physical settlement price of Brent rather than the futures front month, the credit default swap spreads on Gulf sovereign debt — as proxies for ground-level reality rather than relying on headline parsing.

Where Things Stand

As of 12 May 2026, the ceasefire formally remains in place but has been violated by both sides. The one-page MOU framework, which represented the most significant diplomatic progress since the war began, appears to have broken down over the uranium removal clause and Iran’s failure to explicitly renounce nuclear weapons pursuit in writing. Trump has publicly described Iran’s proposal as unacceptable and “stupid,” while sources within his administration say he is now more seriously considering a resumption of major combat operations than at any point in recent weeks.

The Iranian side, characterised by Trump as split between moderates willing to deal and hardliners opposed to any concession, has submitted a response framed around a staggered, phased approach — tackling war termination and sanctions relief first, and deferring the nuclear question to later stages. Washington has consistently rejected that sequencing, insisting that nuclear constraints must be part of any initial framework. The parliamentary speaker made clear after Trump’s “massive life support” remarks that Iran remained open to continued talks but had not changed its fundamental position on the sequencing question.

What makes this situation acutely difficult to price is the presence of three distinct possible outcomes, each with radically different market implications, and each carrying meaningful probability. A successful MOU would compress the risk premium sharply but leave tail risks in place until a full deal is ratified. A breakdown leading to resumed US airstrikes would push Brent toward and potentially through $130, accelerate LNG disruption across Europe, and likely trigger safe-haven flows of a magnitude not seen since 2022. A protracted stalemate — the ceasefire nominally intact but the strait effectively closed and negotiations deadlocked — would sustain the current elevated plateau while grinding down the global economy through supply-side inflation with no clear resolution date.

Traders who approach this environment with humility about what cannot be known, clarity about what the structural indicators are actually showing, and discipline about position sizing for binary outcomes will be better served than those who believe the headline flow is sufficient to generate an edge. The ceasefire may be on massive life support. But so is a great deal of the world’s energy supply — and that is not a variable markets can afford to get wrong.