The Cost of Living and the Case for Investing

The Hidden Cost of Doing Nothing: Inflation and the UK Savings Trap

How years of above-target inflation have quietly eroded the real value of cash savings — and why doing nothing is itself a financial decision with measurable consequences.

There is a particular comfort in a savings account balance that never goes down. The number on the screen stays the same, or grows a little each month, and that stability can feel like prudence — like money well managed. But the screen tells only half the story. While the nominal balance holds, the real value of that balance — what it can actually buy — moves constantly, driven by forces that have nothing to do with the account itself. For most of the last four years, those forces have been moving sharply against the saver.

This is not a theoretical observation. It is arithmetic. When prices rise faster than interest payments accumulate, cash loses purchasing power — quietly, gradually, and without any alarm being triggered. No warning appears on a bank statement when inflation outpaces the interest rate. The account does not flash red. The money does not visibly shrink. Yet the erosion happens all the same, compounding year after year in ways that are easy to ignore and surprisingly difficult to recover from.

Understanding why this happens, and how much it matters, is not simply an exercise in economic literacy. It is the foundation of a rational approach to personal finance. Once the maths is visible, the decision to leave money in a low-rate account ceases to feel like the cautious option. It begins to look, more accurately, like a choice — one with a quantifiable cost.

The Mechanics of Purchasing Power

Inflation is the rate at which the general price level of goods and services rises over time. It is measured in the United Kingdom primarily through the Consumer Prices Index, compiled monthly by the Office for National Statistics. The ONS constructs a theoretical basket of goods and services — food, energy, clothing, housing costs, transport, recreation — and tracks how the price of that basket changes from one year to the next. When the basket costs more this month than it did twelve months ago, inflation is positive. When that rate is high, money’s purchasing power erodes quickly.

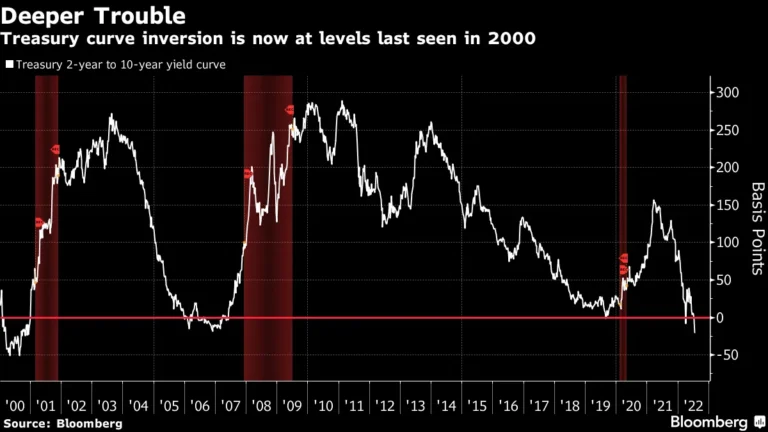

The Bank of England operates with a formal mandate to keep CPI inflation at 2% per year. At that rate, money loses roughly half its purchasing power over about 35 years — a slow and manageable attrition that allows savers to plan with reasonable confidence. But the 2% target is a goal, not a guarantee, and for an extended period beginning in 2021 it was substantially missed. CPI was running below 1% in early 2021, but by the end of that year it had risen to around 5%. Through 2022 it accelerated sharply, driven by pandemic supply chain disruptions, surging energy costs, and Russia’s invasion of Ukraine, reaching a 41-year peak of 11.1% in October 2022. The UK then experienced seven consecutive months of double-digit inflation. Even as the rate gradually declined through 2023 and into 2024, it remained above target — averaging around 6.8% for the full year in 2023. By 2025 it had settled back to an average of approximately 3.4%, still materially above the 2% mandate.

The cumulative effect of that sustained above-target period is striking. According to analysis using ONS data, UK consumer prices increased by more than 20% over the three years from 2021 to 2024. What cost £100 in 2021 cost over £120 by 2024. That is not a rounding error or a minor inconvenience — it is a structural shift in what money buys, and it applies to every pound sitting idle.

The relationship between inflation and interest rates sits at the heart of the savings problem. When the two are in rough alignment — when savings accounts pay roughly what inflation erodes — the saver breaks even in real terms. Their nominal balance grows, but the purchasing power of that balance stays roughly constant. When inflation materially exceeds the savings rate, however, the saver falls behind. The gap between the two rates is the real return, and for much of the period from 2021 to 2024, that real return was deeply negative for anyone holding money in a standard easy-access account.

When Doing Nothing Had a Price Tag

To understand the trajectory of the savings trap, it helps to trace the numbers year by year. In 2021, the Bank of England base rate sat at just 0.1% — a level it had maintained since the early days of the pandemic in March 2020, and the lowest in the Bank’s 327-year history. Commercial banks passed little of even that meagre rate on to savers. The average interest rate on instant-access deposits was approximately 0.06% in April 2021. Inflation, meanwhile, had just begun its ascent, ending the year at around 5%.

The Bank began raising the base rate in December 2021, initiating a tightening cycle that would eventually comprise fourteen consecutive increases over roughly twenty months, taking the base rate from 0.1% to 5.25% by August 2023. But there was a critical asymmetry in how this played out. Banks were quick to pass higher rates on to mortgage borrowers. They were considerably slower to do so with savings accounts. Through most of 2022, when CPI was running between 7% and 11%, average easy-access savings rates remained well below 1%. Even by the peak of the tightening cycle in mid-2023, when headline rates had risen substantially, the average instant-access account was paying around 1.5% to 2% — still a fraction of the prevailing inflation rate.

This is not coincidental. Banks fund themselves partly through retail deposits and have structural incentives to offer savers as little as they can while still retaining their balances. The inertia of savers — the tendency to stay with a familiar provider rather than switching — is well documented and commercially exploited. Research published in 2025 found that as many as one in four UK savers have never switched savings accounts, with many leaving money in accounts paying substantially below market rates. Even at the market peak for savings rates in early 2024, when the average instant-access rate reached approximately 2.82%, inflation was still running ahead of that figure for many savers.

— INSERT IMAGE BLOCK HERE —

A glass jar of coins on a kitchen windowsill — domestic, warm, slightly melancholy. Soft natural light. Hero image for the article.

Making the Maths Visible: £10,000 Over Five Years

Abstract percentages have a way of dissolving before they become real. The clearest way to understand the savings trap is to run the numbers on a specific sum — a round figure that is recognisable as genuine savings — and track what happens to its real value over time under different assumptions.

Consider £10,000 placed in a typical easy-access savings account in January 2022. At that point, the Bank of England base rate was 0.25% and the average easy-access savings rate was approximately 0.2%. CPI inflation for 2022 would eventually average out at around 7.9% for the full year. The saver earned roughly £20 in interest over the first twelve months. Inflation, meanwhile, eroded the purchasing power of that £10,000 by approximately 7.9%, or £790 in real terms. The account nominally contained £10,020 at the end of year one. But in terms of what that money could actually buy, it was worth closer to £9,260 — a real loss of around £740.

Year two brought some improvement in the nominal rate, as savings accounts gradually began to reflect the Bank’s tightening cycle, but inflation remained elevated. In 2023, CPI averaged around 6.8%. Even with savings rates rising toward 1.5% to 2% for diligent switchers — and far less for those who stayed in their existing account — the real return remained substantially negative. A saver who left their £10,000 in a standard account through 2023 might have earned approximately £150 to £200 in interest while losing another 5% or more of purchasing power.

By the end of a three-year period running from January 2022 to December 2024, a saver holding £10,000 in a typical easy-access account would have accumulated modest nominal interest — perhaps £400 to £600 in total, depending on the account and whether they made any effort to seek better rates. But against cumulative CPI inflation of roughly 20% over that period, their real purchasing power would have fallen to approximately £8,600 to £8,700 in 2022 terms. The account balance might show £10,500. The actual buying power is closer to £8,600. The gap — around £1,400 to £1,900 — is the cost of doing nothing.

Nominal balance (account shows)

Real value (purchasing power in 2022 £)

A five-year view extends the picture further. Even as inflation moderated through 2024 and 2025 — averaging approximately 2.6% and 3.4% respectively — savings rates for easy-access accounts were still not keeping pace. The average instant-access rate was 2.12% as of early 2026, against a CPI of 3.0% to 3.3%. The real return remained negative. A saver who placed £10,000 into a standard easy-access account in January 2022 and left it untouched would, by the end of 2025, have a nominal balance of approximately £10,650 to £10,700. But in real terms — measured against what that money could actually purchase — the figure would be closer to £8,300 to £8,400. The nominal gain of around £680 masks a real loss of approximately £1,600.

Research by the personal finance comparison site Finder quantified this dynamic across the UK savings population. Looking at the period from June 2020 to June 2025, the average UK savings account lost approximately £2,989 in real terms. Given that the average UK adult holds just over £16,000 in savings, the study found that savings rates had not kept pace with inflation, meaning the average saver’s pot was worth nearly £3,000 less in real purchasing power than it would have been had interest matched price rises.

Why Banks Captured the Upside and Savers Bore the Cost

The gap between the Bank of England base rate and actual savings account rates — sometimes called the “savings transmission problem” — was a recurring theme of the post-2021 tightening cycle, and it did not go unnoticed by policymakers. The Financial Conduct Authority wrote to major high-street banks in 2023 expressing concern that savings rates were not being passed on to consumers at a pace commensurate with base rate increases. The Treasury Select Committee examined the issue. Comparison websites highlighted the stark difference between the rates offered by high-street incumbents and those offered by newer challenger banks and building societies. Yet the structural reality persisted: the largest retail banks, with their established customer bases and deep deposit pools, had little commercial incentive to rush.

The persistence of inertia among savers is well evidenced. Switching a savings account requires little more than filling in a form, yet roughly a quarter of UK savers have never done it. The same Moneyfacts data that showed average easy-access rates at 2.12% in early 2026 also showed the best available easy-access rates at 4.75% — a gap of nearly 2.6 percentage points that represents hundreds of pounds annually for a saver with meaningful balances. Staying put is a choice, even when it does not feel like one.

The point here is not to single out the banks for criticism or to suggest that savers were somehow negligent. It is to establish that the system does not automatically reward passivity. Inflation is an active force. Savings rates are a commercial product with variable pricing. The combination of the two, across a period of unusually high price pressure, produced a real-terms outcome for many UK savers that they would not have accepted had it been presented explicitly — as a charge deducted from the account, rather than as a purchasing-power loss accrued invisibly over time.

The Numbers in Plain Terms

Between September 2022 and March 2023, the UK experienced seven consecutive months of double-digit CPI inflation, peaking at 11.1% — the highest reading since 1981. Against an average easy-access savings rate of well under 1% through most of that period, the real return on a typical instant-access account was approximately negative 10 percentage points per year. That means every £10,000 sitting in a standard account was losing around £1,000 of purchasing power annually, with no statement, no alert, and no visible deduction.

Investment as a Rational Response

Once the inflation arithmetic is visible, a question follows almost immediately: if cash savings persistently underperform inflation, what is the alternative? The honest answer is that there is no risk-free alternative that reliably beats inflation over all time periods. But the honest framing of the question also requires acknowledging that cash is not risk-free either. The risk of holding cash is inflation risk — the certainty of losing real value at whatever rate prices happen to be rising. That risk simply does not trigger the same emotional response as the risk of watching a portfolio decline in a falling market. It operates silently, which makes it easier to ignore.

Investment in equities, property, or diversified funds does not guarantee a positive real return in any given year. Markets fall, sometimes sharply and for extended periods. But the long-run record of equity markets as an inflation hedge is considerably more robust than that of cash. The FTSE 100 index, including reinvested dividends, delivered a total return of approximately 85% in the decade from 2015 to 2025, equivalent to roughly 6.4% per year on an annualised basis. Over the same period, cumulative CPI inflation was substantially lower. The real return from the index, though volatile, was meaningfully positive.

It is also worth noting the composition of returns over the most recent inflationary episode. FTSE 100 total returns for 2021 were approximately 18.4%, against CPI of around 2.5% — a strong real positive. In 2022, with inflation running at 7.9%, the FTSE 100 still returned approximately 4.4% in total return terms. That was a negative real return, but a far smaller one than the real loss incurred by cash savers. In 2023, the index returned around 7.1% against CPI of 6.8% — roughly break-even in real terms. The 2025 total return was approximately 22.8%, the best in over a decade.

FTSE 100 total return (incl. dividends)

UK CPI annual rate

Past performance does not predict future returns — that caveat is not a formality but a genuine constraint on how confidently any of these numbers should be projected forward. Markets can fall sharply, and they do. But the comparison is instructive not because equities are guaranteed to beat inflation, but because they have historically offered exposure to economic activity and corporate earnings growth that, over meaningful time horizons, tends to track or exceed price increases. Cash, by contrast, offers no such exposure. Its return is fixed by the rate the bank chooses to pay, and as the last five years have demonstrated, that rate is almost never set with the saver’s purchasing power in mind.

Framing the Decision Correctly

The implication is not that every saver should immediately convert their cash holdings into equity investments. That would be a crude misreading of what the maths actually shows. Emergency funds belong in accessible accounts. Short-term savings — money needed within one to three years for a specific purpose — should not be placed in volatile assets that may be worth less at the moment they are needed. These are well-established principles of personal finance planning, not caveats to be dismissed.

The implication is narrower and more specific: money that has no near-term purpose, held in low-rate accounts for years or decades because the account holder has not yet decided what to do with it, is not sitting safely. It is eroding. The decision not to invest is itself a financial decision, and it carries a cost that is just as real as the risk of a portfolio decline — it simply does not look like a loss on any statement.

Longer time horizon

Money not required for three years or more has time to absorb short-term market volatility while pursuing a real return above inflation. The longer the horizon, the stronger the historical case for equities over cash.

Shorter time horizon

Money needed within one to two years should remain in accessible cash, with the focus shifted to finding the best available savings rate rather than accepting the default from an incumbent bank.

The ISA wrapper

Stocks and Shares ISAs allow equity investment up to £20,000 per year with all returns — capital growth and dividends — sheltered from UK income and capital gains tax. The wrapper does not eliminate volatility, but it removes a significant tax drag on long-term returns.

Switch your cash account

For money that genuinely belongs in cash, the gap between the best and worst available easy-access rates can exceed 2.5 percentage points. At current average savings rates, the difference on a £10,000 balance represents over £250 per year — more than a negative real return requires.

The UK savings landscape of 2022 to 2026 offers an unusually clear case study in the cost of monetary passivity. It was not a period of financial crisis, stock market collapse, or economic catastrophe — it was simply a period in which prices rose faster than the default return on money in a standard account. That combination is not unusual in the historical record. It is, in fact, more common than its opposite. The 2010s — a decade of near-zero interest rates and subdued inflation — were the anomaly, not the norm. The recent experience is a return to a more historically typical relationship between cash and inflation, one in which holding money without a purpose has a measurable cost.

The argument for investment is not that markets always go up, or that risk can be eliminated, or that any particular asset class is the right choice for every individual. It is simply this: doing nothing is not neutral. In a world where prices rise over time, the question is never whether to accept risk — it is which risk to accept. The invisible, steady erosion of purchasing power or the visible, temporary volatility of a diversified portfolio. That is the real choice on the table, and understanding it clearly is the first step to making it deliberately.